原文题目:Beyond carbon pricing: The role of banking and monetary policy in financing the transition to a low-carbon economy

原文作者:Emanuele Campiglio

作者单位:Grantham Research Institute, London School of Economics, Houghton Street, London, United Kingdom

期刊名:Ecological Economics

月份:Available online 27 March 2015

关键词:绿色投资、银行、信用创造、绿色宏观审慎监管、货币政策

文献综述

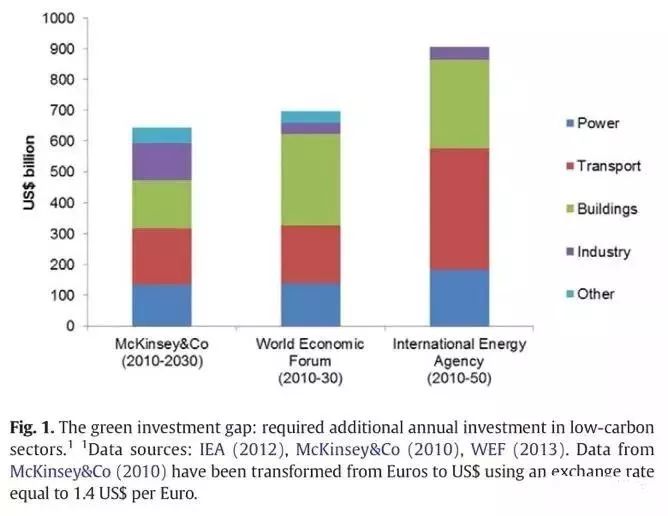

实现绿色经济转型,需要调动经济资源流向低碳生产部门,但对低碳部门的投资还远远低于实际需求。图1说明了一些机构和学者对全球“绿色投资缺口”的估计,刻画出在能源、交通、建筑、工业等领域绿色投资的不足。想要弥补这些资金缺口,最主要障碍就是由环保公共产品缺乏市场定价而带来的市场失灵。因此,引入碳定价成为吸引私人投资者参与绿色投资的前提条件。目前,碳定价最主流的方法有两种:一是碳排放税,二是碳排放许可证。

然而本文提出,只依靠碳定价本身是不够的,即使是一个稳定而可靠的碳定价体系也不能解决低碳部门的“信贷市场失灵”。低碳企业需要信贷来支持相应的项目,但后金融危机的时代背景下,哪怕存在有潜力的投资机会和价格信号,商业银行可能也没有信心创造新的信用。低碳项目大多风险高且周期长,再加上碳定价政策的不确定性,商业银行往往不愿意进行投资。因此,银行监管机构还需要一些不依靠价格的政策来缓解信贷市场失灵。

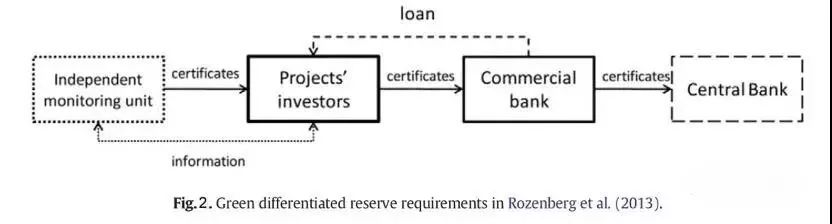

针对这种情况,本文重点论述了货币政策和绿色宏观审慎监管的潜在作用。例如,根据资金流向实行差别化存款准备金率,贷款给低碳部门的银行可以获得低于平均的准备金率。假定银行通过贷款获得利润,降低准备金率扩大了银行能创造的潜在信用,那么这个政策就使得商业银行更有动力把资金引入绿色领域。按照Rozenberg et al. (2013),政策运行机制如图2所示:首先,一个有低碳项目的企业把项目细节汇报给独立的监管机构(如环保局),核算出该项目能带来的减排量并授予相应的证书。然后,企业再去申请贷款,并把证书上交给商业银行。最后,商业银行把这些证书作为准备金的一部分,上交给央行。目前,黎巴嫩已经开始实施名为“国家能源效率与新能源行动”(National Energy Efficiency and Renewable Energy Action, NEEREA)的计划,基本思路就是实行差别化准备金率。其他的绿色宏观审慎监管政策,例如差别化资本充足率、“窗口指导”等,也有一些国家正在进行尝试。

那么,这类政策在现实中到底是否有用呢?本文给出的回答是,对于新兴经济体是有用的。在高收入的发达国家,参考利率几乎是过去十多年里唯一的政策工具,而准备金率实际上已经不能对银行的借贷行为产生约束。但新兴经济体往往对信贷分配有更强力的控制,也允许更多货币政策工具的运用,包括对资本流动性比、贷款价值比、债务收入比等设定上限,对利润分配进行规定等。以中国为例,从2008年起中国人民银行就根据商业银行的规模,实行两档差别化准备金率,小银行的准备金率更高,而大银行的准备金率更低。总之,货币政策和绿色宏观审慎监管在新兴经济体中更加可行,更能引导银行的绿色投资。

Abstract

It is widely acknowledged that introducing a price on carbon represents a crucial precondition for filling the current gap in low-carbon investment. However, as this paper argues, carbon pricing in itself may not be sufficient. This is due to the existence of market failures in the process of creation and allocation of credit that may lead commercial banks — the most important source of external finance for firms — not to respond as expected to price signals. Under certain economic conditions, banks would shy away from lending to low-carbon activities even in the presence of a carbon price. This possibility calls for the implementation of additional policies not based on prices. In particular, the paper discusses the potential role of monetary policies and macro-prudential financial regulation: modifying incentives and constraints that banks face when deciding their lending strategy — through, for instance, a differentiation of reserve requirements according to the destination of lending— may fruitfully expand credit creation directed towards low-carbon sectors. This seems to be especially feasible in emerging economies, where the central banking framework usually allows for a stronger public control on credit allocation and a wider range of monetary policy instruments than the sole interest rate.

文献整理:丁小筱

来源:复旦绿金

转自:复旦绿金